📅 June 2026 | ✍️ Mitti Gold Organic | 🗂️ Legal

📥 Download Sample Format

Get the sample document format in English, Hindi, Gujarati, or Urdu.

Understanding the Loan Burden (Bhoja) on Agricultural Land

For millions of farmers, accessing institutional credit through agricultural loans—whether for purchasing seeds, fertilizers, tractors, or installing irrigation systems—is a fundamental necessity of modern farming. When a bank or cooperative society sanctions an agricultural loan, they require collateral to secure the debt. In the vast majority of cases, the farmer's agricultural land serves as this collateral. To legally formalize this lien and protect the lender's interests, a formal entry is made in the official land revenue records, specifically on the 7/12 extract (Satbara Utara) and the 8-A account booklet. This entry is commonly known as a \"Bhoja\" (burden or encumbrance) or a \"Gahan\" (mortgage) entry. As long as this entry exists in the \"Other Rights\" (Itar Hakka) column of your 7/12 extract, the land is legally encumbered. The bank holds a statutory charge over the property, meaning you cannot legally sell, transfer, or subdivide the land without the explicit, written consent of the lending institution. Understanding that this entry is a strict legal hold on your property is the crucial first step in realizing why its prompt removal upon loan repayment is absolutely essential for your financial freedom.

Why Removing the Loan Entry is Crucial

A common, yet highly detrimental, mistake made by many landowners is assuming that paying the final installment to the bank automatically clears their land title. Repaying the bank and updating the revenue records are two entirely separate administrative processes. The bank will close your account, but the revenue department will not remove the Bhoja until they receive a formal application and the appropriate clearance documentation. Leaving a repaid loan recorded as an active burden on your 7/12 extract has severe consequences. Primarily, it severely cripples the marketability of your land. No prudent buyer will purchase, and no competent lawyer will clear the title for, agricultural land that shows an active bank lien. Furthermore, if you need to apply for a new crop loan for the upcoming season from a different financial institution, they will pull your 7/12 extract. Seeing the existing burden, they will immediately reject your new loan application, assuming you are already over-leveraged. Therefore, removing the burden is not just a housekeeping task; it is a mandatory legal procedure to restore your absolute ownership rights and regain your financial agility.

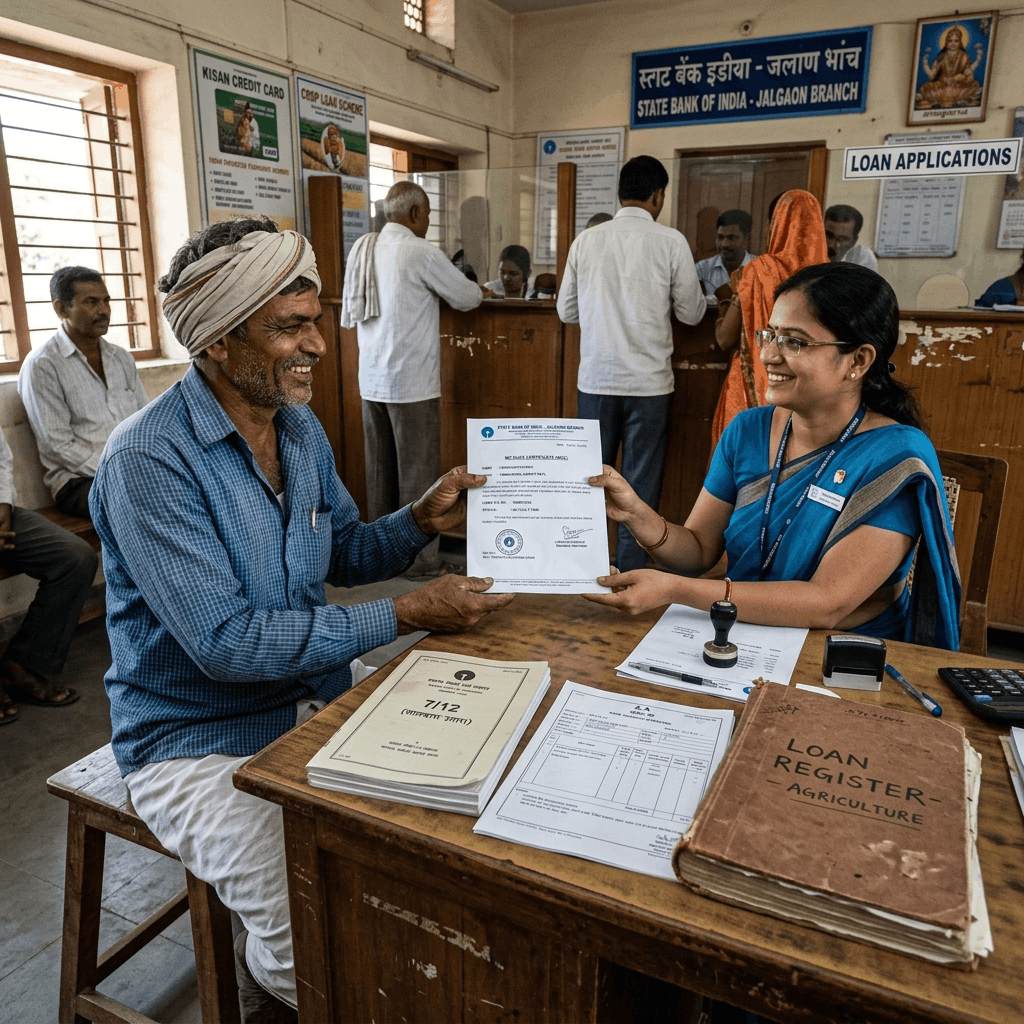

The Process of Loan Repayment and Obtaining the No Dues Certificate

The bureaucratic process of removing the burden can only commence after the underlying financial obligation has been completely extinguished. You must first ensure that the entire principal amount, all accrued interest, and any applicable penal charges or processing fees have been paid in full to the lending institution. Once you make the final payment, you must explicitly request the bank to formally close the loan account. The critical document you must obtain from the bank manager is the \"No Dues Certificate\" (NDC) or the \"Loan Closure Letter.\" This is an official document, issued on the bank's formal letterhead, bearing the bank's seal and the authorized signature of the manager. It explicitly states your name, the specific loan account number, the details of the mortgaged property (Gut number/Survey number), and crucially, a categorical declaration that the loan has been repaid in full and the bank no longer holds any claim or lien over the specified land. This NDC is the cornerstone of your application to the revenue department; without a valid, original NDC, the Talathi will refuse to even initiate the process of removing the burden.

Key Documents Required for Loan Removal Application

When approaching the revenue authorities to update your land records, you must present a complete and legally sound set of documents. Bureaucratic delays are almost always caused by incomplete paperwork. The primary document, as discussed, is the original No Dues Certificate (NDC) issued by your bank. You must also submit a formal, written application letter addressed to the Talathi (Village Accountant) or the Tehsildar, explicitly requesting the removal of the specific Bhoja. You will need to attach the latest, digitally signed copies of the 7/12 extract and the 8-A extract; these copies clearly show the active loan entry that you are seeking to remove. Identity proof is mandatory, so attach clear photocopies of your Aadhaar card and PAN card. If the original loan was taken by multiple co-owners, or if it was an ancestral loan and the original borrower is deceased, you will need additional documentation, such as death certificates and legal heirship certificates, to prove your legal standing to make the application. Ensure you keep photocopies of the entire application packet for your personal records before submitting the originals to the revenue office.

Drafting the Formal Application to the Talathi or Tehsildar

The formal application letter is the administrative trigger that initiates the mutation process. It must be drafted clearly, concisely, and contain all necessary legal particulars. Address the letter to the competent revenue authority—usually the Talathi of your specific village or the Circle Officer. The subject line should clearly state: \"Application for the Deletion of Loan Burden (Bhoja) from 7/12 Extract.\" In the body of the letter, provide your full name and residential address. Crucially, explicitly mention the specific details of the land: the Village name, the Taluka, the District, and the exact Gut Number (or Survey Number) as it appears on the 7/12 extract. State the details of the loan, including the name of the bank, the branch, the date the loan was recorded, and the exact amount of the burden currently showing on the record. Finally, state that the loan has been fully repaid, reference the attached No Dues Certificate, and formally request that the mutation entry (Ferfar) be initiated to delete the bank's name from the \"Other Rights\" column. A well-drafted application prevents confusion and accelerates processing.

Step-by-Step Guide to the Online Application Process

In recent years, many Indian states have aggressively digitized their land revenue systems, making it possible, and often mandatory, to initiate the burden removal process online through official state portals (like Mahabhumi in Maharashtra). To apply online, you generally need to create an account on the state's land records portal using your Aadhaar number and mobile number for OTP verification. Once logged in, navigate to the e-Mutation (e-Ferfar) section and select the specific service for \"Removal of Bhoja/Encumbrance.\" The system will prompt you to enter your district, taluka, village, and Gut number. It will then fetch your current 7/12 details. You will need to fill out an online form detailing the loan closure and upload scanned PDF copies of your application letter, your Aadhaar card, and most importantly, the bank's No Dues Certificate. After submitting the documents, you will usually be required to pay a nominal processing fee through an online payment gateway. Upon successful submission, the system will generate a unique application acknowledgment number. This number is vital; it allows you to track the real-time status of your application as it moves from the Talathi to the Circle Officer for approval.

The Role of the Bank or Cooperative Society in the Process

While the farmer initiates the process, the bank or the cooperative credit society plays a crucial verifying role. To prevent fraud (such as a farmer forging a No Dues Certificate to illegally clear their title), the revenue department will not simply take your submitted NDC at face value. When the Talathi initiates the mutation entry (Ferfar) to remove the burden, standard administrative procedure dictates that an official notice (commonly known as a Section 135D notice under the Maharashtra Land Revenue Code) is generated and sent to all interested parties, which strictly includes the lending bank. The notice informs the bank that an application has been made to remove their lien based on a claim of loan repayment. The bank is given a specific statutory period (usually 15 to 30 days) to raise any formal objections. If the loan is indeed fully repaid, the bank will ignore the notice or send a formal \"No Objection.\" However, if there are outstanding dues, the bank will immediately file an objection, instantly halting the mutation process. Maintaining good communication with your bank manager and informing them that the revenue department will be sending a verification notice can help ensure they process it without delay.

Understanding the 7/12 Extract and Mutation Entries (Ferfar)

To navigate this process confidently, you must understand how the revenue records mechanically function. The 7/12 extract is not a static document; it is a dynamic record that reflects the current legal status of the land. Any change to this status—whether a sale, an inheritance, placing a loan burden, or removing a loan burden—must go through a formalized process called a \"Mutation\" or \"Ferfar.\" When you submit your application and the NDC, the Talathi does not immediately erase the bank's name. Instead, they create a new Mutation Entry (Ferfar) proposing the deletion of the burden. This entry is recorded in the Mutation Register. The previously mentioned notices are sent out based on this Ferfar. Only after the statutory notice period expires without any valid objections from the bank or other parties does the Circle Officer (Mandal Adhikari) review the file. If everything is legally sound, the Circle Officer will officially \"certify\" or approve the Ferfar. It is only at the precise moment of certification that the bank's name is finally struck off the actual 7/12 extract, rendering your title clean.

Navigating the 8-A Khate Pustika Updates

While much of the focus is on the 7/12 extract, farmers must not neglect the 8-A extract. The Form 8-A is essentially the farmer's holding account ledger; it aggregates all the different parcels of land (Gut numbers) owned by that specific individual within the village and calculates the total land revenue tax payable. Just as a loan burden is recorded on the specific 7/12 extract of the mortgaged land, an aggregate note of the farmer's indebtedness is often made in their 8-A Khate Pustika. It is vital to ensure that when the mutation process clears the Bhoja from the 7/12 extract, the corresponding entry in the 8-A register is also concurrently updated by the Talathi. A mismatch between a clean 7/12 and an encumbered 8-A can cause severe bureaucratic confusion down the line, particularly when applying for state agricultural schemes or comprehensive crop insurance that require a clean, unified profile of the farmer's total land holdings. Always explicitly verify that both documents reflect the updated, debt-free status.

Common Delays and How to Overcome Them

Despite clear procedures, applications to remove loan burdens frequently face frustrating delays. One of the most common causes is a discrepancy in the spelling of the farmer's name or the exact Gut number between the bank's No Dues Certificate and the official revenue records. The revenue department operates on strict exactitude; even a minor typo will cause the Talathi to reject the NDC. To overcome this, verify all details meticulously before leaving the bank; if there is an error, demand a corrected NDC immediately. Another major cause of delay is the physical transmittal of the 135D objection notices to the bank. Sometimes these notices are lost in transit or sit unread on a bank manager's desk. You can proactively overcome this by obtaining a physical copy of the notice from the Talathi and hand-delivering it to the bank manager, requesting them to formally acknowledge receipt and immediately issue a written \"No Objection\" letter directly to the revenue office. Proactive, polite, and persistent follow-up at both the bank and the Talathi's office is the most effective strategy against bureaucratic inertia.

Legal Recourse in Case of Bank Refusal or Delay

In rare but highly stressful situations, a farmer may fully repay the loan, yet the bank unreasonably delays issuing the No Dues Certificate or wrongfully refuses to release the lien due to administrative errors or disputes over minor hidden charges. If you find yourself in this predicament, you have legal recourse. First, escalate the issue formally by writing a registered grievance letter to the Bank's Branch Manager and the Regional Manager, detailing the repayment history and demanding the NDC. If the bank remains unresponsive after 30 days, you should file a formal complaint with the Banking Ombudsman appointed by the Reserve Bank of India (RBI). The Ombudsman has the authority to mandate the bank to issue the clearance certificate and can even impose penalties on the bank for deficiency in service. Furthermore, an unreasonable refusal to release a mortgage after full repayment constitutes a severe deficiency in service under the Consumer Protection Act. You have the right to file a case in the District Consumer Disputes Redressal Forum, seeking an order directing the bank to issue the NDC and claiming financial compensation for the mental agony and any subsequent financial losses caused by the encumbered title.

Ensuring Accuracy of the Updated Records

The process is not truly complete when the Circle Officer approves the mutation; it is only complete when you have visually verified the final result. Once the mutation (Ferfar) to remove the burden is certified, you must immediately apply for a fresh, digitally signed copy of your 7/12 extract and your 8-A extract. Do not assume the system updated correctly. You must meticulously examine the new 7/12 extract. Look specifically at the \"Other Rights\" (Itar Hakka) column at the bottom of the document. The entry detailing the bank's name and the loan amount must be entirely absent, or there should be a specific notation stating that the burden has been removed via the specific Ferfar number. If the bank's name still appears, a critical administrative error has occurred. You must immediately take the certified mutation order back to the Talathi and demand that the computerized record be corrected to reflect the approved order. Failing to verify the final document leaves you vulnerable to discovering the error years later when you desperately need a clean title.

The Impact of Clear Records on Future Loans and Subsidies

Maintaining a completely clean and updated 7/12 extract is not just about administrative tidiness; it has a massive, direct impact on the financial viability and growth potential of your farming operation. When the previous loan burden is officially removed, your land regains its full collateral value. This is crucial because agriculture often requires cyclical borrowing. With an unencumbered title, you can immediately approach any financial institution to secure a new crop loan for the upcoming Kharif or Rabi season, often negotiating better interest rates because you present a lower risk profile. Furthermore, government agricultural departments rely heavily on these records. Many lucrative state and federal subsidy schemes—such as subsidies for installing expensive drip irrigation systems, purchasing heavy tractors, or constructing polyhouses—require the applicant to submit a clean 7/12 extract to prove they have the financial capacity and unencumbered land to utilize the subsidy effectively. A lingering, outdated loan entry will instantly disqualify you from these vital financial support mechanisms.

Dealing with Ancestral Loans and Inheritance Issues

Removing a loan burden becomes significantly more complex when dealing with ancestral property where the original borrower (e.g., a father or grandfather) has passed away. In these cases, the legal heirs inherit not only the land but also the liability of the outstanding loan. To remove the burden, the heirs must collectively clear the outstanding debt. However, the bank cannot issue a No Dues Certificate in the name of a deceased person. The heirs must first complete the inheritance mutation (Varas Ferfar) at the revenue office to get their names officially recorded as the current owners on the 7/12 extract. They must also submit the death certificate and a legal heirship certificate to the bank. Only then will the bank accept the final settlement from the heirs and issue the NDC in the names of the current, legally recognized owners. Handling this sequence incorrectly—trying to clear the bank loan before establishing legal heirship—will result in documents that the revenue department cannot legally process, leading to severe bureaucratic deadlocks.

Conclusion: Maintaining Clean Agricultural Land Records

The diligent maintenance of agricultural land records is a paramount responsibility for every farmer, and ensuring the prompt removal of discharged loan burdens is the most critical aspect of this maintenance. While navigating the revenue department's bureaucracy can sometimes feel tedious and repetitive, leaving an outdated encumbrance on your 7/12 extract is a profound legal liability that restricts your financial freedom and degrades the value of your primary asset. By understanding the strict procedural necessity of the No Dues Certificate, drafting clear and precise applications, embracing the efficiency of online portals where available, and persistently following up on the mutation process through to the final certification, you can secure an absolute, clean title. Make it an inflexible rule of your agricultural business practice: the moment you pay the final installment of a bank loan, you immediately initiate the process to strike that burden from your land records. A clean 7/12 is the foundation of agricultural prosperity.

📦 Bulk Orders & Export

Mitti Gold Organic: For bulk orders of all organic fertilizers — Farmers, Nurseries, and Export. WhatsApp: +91 95372 30173

Frequently Asked Questions (FAQs)

Will the bank automatically update my 7/12 extract once I pay off my loan?

No. This is a very common misconception. The bank will close your account, but it is entirely your responsibility to obtain the No Dues Certificate and formally apply to the revenue department (Talathi) to have the record updated.

What is the most important document needed to remove the Bhoja?

The absolute most important document is the original No Dues Certificate (NDC) or Loan Clearance Certificate issued by the bank manager, explicitly stating the loan is fully repaid.

Who do I submit the application to?

You must submit the application, along with the NDC and your identity documents, to the Talathi (Village Accountant) of the village where the agricultural land is located.

Can I apply to remove the loan burden online?

Yes, in many states, this process is now digitized. You can use the state's official land records portal (e.g., Mahabhumi in Maharashtra) to initiate an e-Mutation request for the removal of the encumbrance.

Why does the Talathi send a notice to the bank after I submit the NDC?

The notice (often called a 135D notice) is a mandatory legal verification step to prevent fraud. It gives the bank an opportunity to object if the NDC is forged or if there are still hidden dues outstanding.